Friends Don't Let Friends Pay High Fees

Friends Don't Let Friends Pay High Fees

Demystifying AUM and Investment Costs

Backstory:

I love attending events and celebrating the success of friends and colleagues. It’s so great to see a light being shined on them, and for me, it is fuel and energy to keep going and find those activities that have meaning and purpose for me.

When I meet new folks at these events, the standard question comes up, “So what do you do?” It’s hard to say. I’m 16 months into retirement and redefining my new life, which includes:

Fellowship - spending more time with family and friends. Life is too short, especially when good people leave this world too soon.

Advocacy – I’m committed to advancing economic empowerment for women and the Hispanic Community. This shows up in a few different ways: speaking, coaching, writing here, and contributing to causes that help advance the platform.

Vocation – learning and growing new modes of thinking, doing, and being.

Enterprise – growing my skills in building something. Honestly, this one keeps morphing and changing as my interests in #1 through #3 are so important to me.

The short answer I give:

I’m working to help close the wealth gap for women.

Folks immediately assume that means I’m a financial advisor.

Oh, so are you a financial advisor?

No, I’m not a financial advisor. For the folks I work with, my goal is to walk side by side with them as they learn and grow their financial courage, skills, knowledge, and capabilities. I share my experiences and insights. And guess what? I learn from them and watch their knowledge and growth flourish. Frankly, this is some of the best parts of the work!

Your Financial Team & the Common Compensation Model

Having a financial advisor on your team can be a good thing as long as there is value alignment and roles and responsibilities are clearly defined by you. We all should have team members on OUR team that can provide advice and guidance. At the end of the day, you are still in charge, and it is your decision and, ultimately, responsibility for what you do with the money you make, spend, keep, invest, and give. I tell folks, "You are the quarterback” and GM of your team. You get to decide who joins when it is time to leave and who you turn to for insights. Then you decide what plays to make and execute in partnership with the appropriate wealth professional (legal, tax, insurance, financial, coach). This financial team model does involve you being knowledgeable of the work as well as being knowledgeable of how you will pay these professionals.

Financial Advisors Compensation Models:

Let’s talk about the financial advisor’s compensation structure – particularly Assets Under Management. This came up in a recent discussion and the fees you could potentially be paying.

AUM – The Short Explanation:

AUM (Assets Under Management) fees are a prevalent fee structure in the investment management and financial advisory industries. AUM fees are typically based on a percentage of the total assets being managed by a financial advisor. The history of AUM fees can be traced back to the early days of the investment management industry when financial advisors were primarily focused on managing investment portfolios for wealthy clients. Today, financial advisors’ roles have expanded to include financial, tax, retirement, cash flow planning and insurance, estate planning, etc.

The Criticism:

There are different camps when it comes to AUM fees. The Do-It-Yourselfers have harsh criticisms of the AUM fee structure, mainly due to:

Potential for conflicts of interest

High costs – especially over long periods of time, and the potential for diminished returns for you, the client.

AUM fees can incentivize advisors to focus on growing assets under management rather than providing the best advice for their clients.

The compounding nature of these fees can result in substantial costs over time.

Penalizing clients for saving and investing, as fees are based on the total assets under management.

Potentially discouraging advisors from recommending strategies that would reduce assets under management, such as paying off debt or investing in employer-provided retirement accounts.

Wealth management can be and is a big business. According to Statista, it is estimated that there were $103 trillion of global assets under management (AUM) as of 2020 (latest data available). Building a business is the American dream. Look for an advisor who is more focused on the services they provide you versus the business they are building to sell one day.

The Benefits:

Despite the criticism, there are benefits to the AUM fee structure. AUM fees align the interests of the advisor and the client to some extent, as advisors benefit from growing the client’s assets. Likewise, AUM fees are simple to understand and can provide clients with a clear understanding of what they are paying for. It’s the simplicity that makes it easy to say yes without digging into the details.

True Financial Costs:

The true financial costs of AUM fees depend on the percentage charged and the length of time the assets are managed. As the AUM fee compounds over time, it can have a significant impact on the client’s returns. If you are not familiar with this concept, now is a great time to learn so you can manage all the fees you are paying and make sure they align with the value you are receiving and understand the long-term impacts.

As a reference, here is an article I sent to a colleague back in December 2014. She was looking for some financial mentoring at the time. This article was striking then and relevant still today on the true costs of AUM fees.

The short of the article is that fees can eat up a good portion of returns as a client. John Bogle argued that over a 65-year horizon, it would be 80% of a client’s potential account balance. Yikes!

An Example:

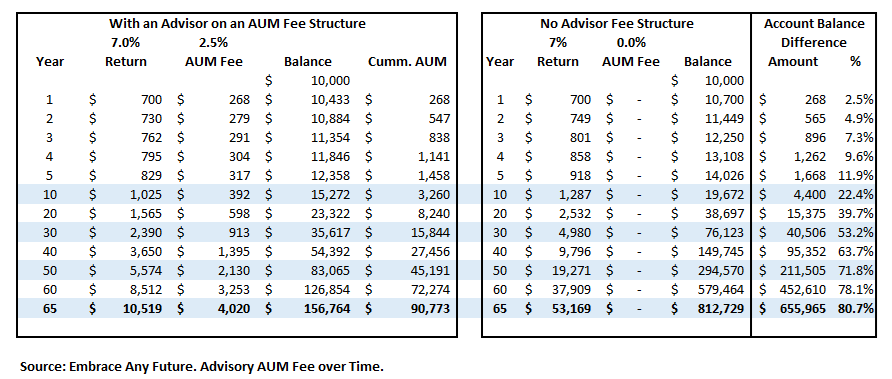

Assume a 20-year investment relationship with a 7% annual return and a 2% AUM fee. The client starts with an initial investment of $10,000.

With a 7% return and no fees, the investment would grow to approximately $38,697. If a 2% AUM fee is applied, the investment would grow to approximately $25,834. In this scenario, the advisor would receive around $6,972, and the account balance would have been $12,863 lower or 33.2% lower than if there were no AUM fees over the 20-year period. The difference between the AUM fee reduction ($6,972) and the total reduction ($12,863) is the lost compounding associated with the AUM fees removed from the account.

Curious about the cost over shorter or longer time horizons? Check out the table created below based on a 7% return and 2% AUM over a 1-year to 65-year time horizon.

Questions You May Ask:

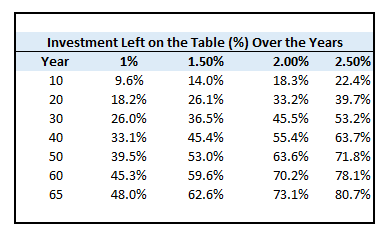

How did Bogle come up with 80% of the total account left on the table? An AUM fee of 2.5% was used over a 65-year period. See the table created below to illustrate his point.

Thanks for sharing, but I don’t plan to be invested for 65 years. What is the impact of lost account values over a shorter horizon?

On a 20-year investing horizon, a 1% AUM fee is worth a reduction of 18.2%. In essence, you are losing 18.2% of your account balance because of the impact of fees. Does it seem material to you?

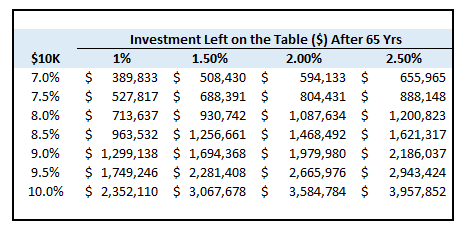

Hey, my advisor is earning me a higher return, which I’m ok with paying the 2% fee. However, I’m curious what the impacts would be on a $10,000 investment.

As you can see, the higher the return on the same AUM percent, the higher (in multiples) the investment balance left on the table due to AUM fees. For example, if you have an 8% return vs. a 7% return with a 1% AUM fee, it results in $323,804 ($713,637 less $389,833) fewer assets.

What other financial advisory fee options are available?

Flat Financial Planning Fee:

an alternative fee structure where clients pay a fixed amount for financial planning services. This fee can be charged annually, semi-annually, or quarterly. Services vary and can include investment management, retirement planning, tax planning, estate planning, risk management, and budgeting.

Benefits:

Greater transparency – Clients know exactly how much they are paying for the services they receive. This is really huge for you emotionally.

No conflicts of interest – Advisors are not incentivized to grow assets under management, allowing them to focus on providing the best advice for their clients.

Cost savings – A flat fee is typically more cost-effective than an AUM fee. You decide when to re-engage for an update.

Criticisms:

Limited alignment of interests – Flat fees may not align the advisor’s interests with the client’s investment performance.

Accommodating – Flat fees may not account for the complexity of a client’s financial situation or the time required to provide advice. To offset, try to keep things simple. Complexity is high maintenance, and that always costs more.

Perception of value – There is a lot involved in putting together a plan. Some clients may perceive the flat fee as expensive if they do not fully understand the scope of services provided.

Costs:

For comprehensive financial planning fees, the fee can vary based on the complexity of the client’s financial situation and the specific services provided. Generally, clients with higher assets may pay a higher flat fee due to the increased complexity of their financial planning needs. Per Kitces 2020 Financial Advisor Report, flat fees range from $2,500 to $7,500. I’ve seen them even higher at $10,000+

Hourly fees: Financial advisors who charge an hourly fee typically charge between $200 and $300 per hour.

Hybrid Fee Models: in response to the criticisms and limitations of both AUM fees and flat financial planning fees, some advisors have adopted hybrid fee models, which combine elements of both fee structures to create a more balanced and customizable approach to financial planning and investment management.

Tiered AUM Fee Structure - A common hybrid fee model where the percentage charged decreases as the assets under management increase. This model can incentivize advisors to grow their clients’ assets while still providing a more cost-effective fee structure for high-net-worth clients. This has become more common in the last 10 years. You should expect to see a tiered structure. Just pay close attention to the tiers. Sometimes you are still paying 2% because your balance is not large enough to warrant the decreased fee structure. Review the tiered fee table to the costs you will ultimately pay noted in the tables above.

The specific fees charged by advisors can vary widely depending on factors such as the advisor’s experience, the complexity of the client’s financial situation, and the level of service provided. AUM Fees, the percentage charged, tend to decrease as the assets under management increase. However, here is a general market insight:

$1M in assets: 1.0% - 1.5% AUM fee

$2M in assets: 0.75% - 1.25% AUM fee

$3M in assets: 0.50% - 1.0% AUM fee

Flat Fee + Lower AUM Fee - clients pay a fixed fee for financial planning services and a separate, lower percentage for assets under management. This model can provide greater transparency and reduce conflicts of interest while still aligning the advisor’s interests with the client’s investment performance.

In hybrid fee models, the fees can be a combination of tiered AUM fees or a combination of flat fees and AUM fees, as mentioned earlier. The specific fee structure will depend on the advisor’s approach and the client’s preferences. All I’ll say is pay close attention to anything that is tied to your account balances. Compounding is a powerful tool that can work for you or against you – even with the best of intentions by you and your advisor.

Other Investment Fees to be aware of.

Here are other fees associated with public company investments you should be familiar with and manage as best as possible.

Brokerage fees: These are fees charged by brokers for executing trades on behalf of investors. They can be charged as flat fees or as a percentage of the trade value.

Mutual fund fees: These fees are associated with managing and operating mutual funds. They include expense ratios, which cover management fees, administrative expenses, and other costs, and sales charges or loads, which are fees paid when buying or selling fund shares.

Exchange-traded fund (ETF) fees: ETFs charge an expense ratio similar to mutual funds, but they usually have lower fees. They also involve brokerage commissions when buying or selling shares.

Retirement account fees: These fees are associated with retirement accounts like 401(k) plans and individual retirement accounts (IRAs). They can include administrative fees, investment fees, and individual service fees.

Miscellaneous fees: Additional fees can be associated with investment accounts, such as account maintenance fees, inactivity fees, and transfer fees.

Next Steps:

Review your taxable, tax-deferred, and tax-free accounts across all your brokerage providers to determine the fees you are already paying. Go to your “activities” section and review for the last 18 months. See what you are paying in fees relative to the account balances. While you might not have an advisory fee, you could have other fees you are not aware of. Review your 2022 Year End reports seeing all the activities.

If you invest in funds, review the expense ratios. I noticed recently some money market funds are carrying a .42% expense ratio. It seems awfully high relative to other options that offer low-risk/risk-free rates.

Determine if this makes sense for you. The costs seem high, as we just demonstrated, for a low/no-risk solution.

3) Read the article “If you are a Saver, you are an Investor. This article was written in January 2023, ahead of the Silicon Valley Banking crisis. Learn the basics of the business of banking and determine your investment strategy for your cash on hand. Keep an eye out for those high-fee money market funds. Also, keep in mind, you are already an investor.

Summary:

Fees are just as important as returns. We cannot control our returns, but we can best manage our investment fees. Consider your own financial situation and preferences when deciding which fee structure(s) are right for you.

Happy Fee Hunting!