Navigating an Economic Slowdown and Credit Crunch

Navigating an Economic Slowdown and Credit Crunch

A Personal Reflection on Cash Management for Businesses & Non-Profits

Over the last few months, I've been on a personal journey of reviewing small businesses to buy, diving into financials, and connecting with business owners, M&A attorneys, and finance brokers. Alongside this, I enrolled in an M&A course at Columbia Business School to deepen my understanding of deal construction, consideration, and risk mitigation.

Amidst these experiences, the rapid collapse of Silicon Valley Bank served as a stark reminder of the importance of cash management in business. As someone who genuinely cares about the well-being of business leaders, businesses, non-profits, and the economy, I want to emphasize the significance of cash flow for maintaining stability, driving growth, and improving business valuation during a sale.

Why It Matters

We find ourselves in the midst of a credit crunch, with banks slowing down lending and large companies imposing long credit terms (60 to 90 days), which significantly impact smaller businesses. We all know those companies that feel compelled to place such terms on smaller businesses. Further, recent off-the-record comments suggest that regulators may be asking banks to slow down lending even more. Yet, go to any restaurant, and you see the room bustling with business. It can be confusing. However, I would say, now, more than ever, cash management is crucial for businesses to thrive and stay afloat.

In my personal experience, mid-level leaders in large institutions (corporations, state, and local governments) often don’t worry about cash, as those who do tend to keep their concerns quiet in order to provide a sense of stability for the company and its employees. This can create a false sense of security. For small business owners, being more steadfast and determined in maintaining stability for their company and employees is crucial, and cash management is the solution.

Big Picture

Cash management should be a general priority 365 days a year—not only a priority during a crisis. Small business owners should be proactive in addressing potential cash flow issues and openly discussing cash processing opportunities with their teams to help drive the change needed. Process improvement creates a more resilient business environment.

What You Can Do

To stay ahead of potential cash flow issues, I encourage you to analyze your own cash management strategies. There are over 75 cash management strategies and analyses available to help improve your company or non-profit’s financial position. The time to start is now.

Strategies to Consider

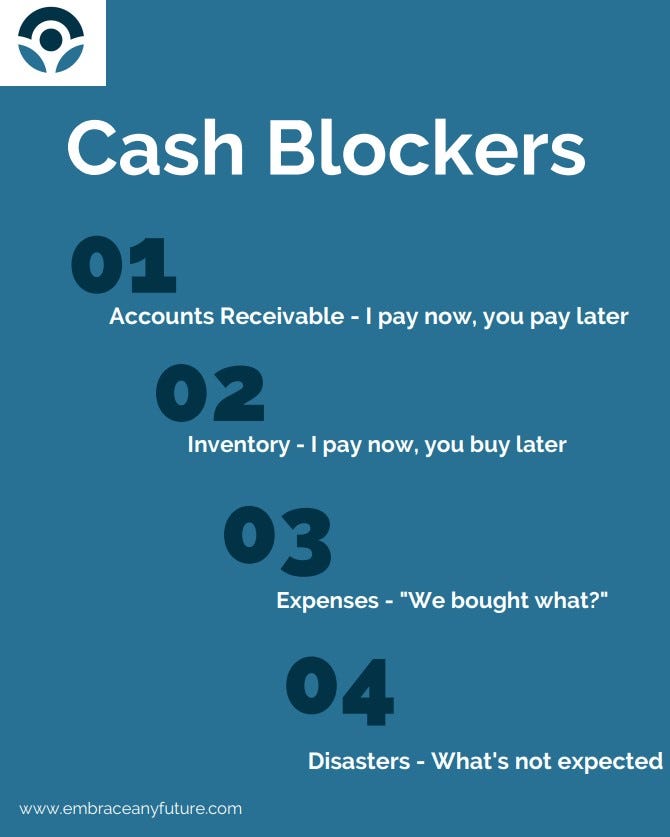

Timing of billing - how long do you wait to bill?

Days and efforts to collect - it costs more than you think if you have slow payers.

Degree of maintenance of clients who pay late. If you are waiting 60 to 90 days and are calling with no result, collect and then let the client know it’s time they seek another solutions provider.

Review your pricing - are all costs covered by revenue with some extra left over?

Inventory size or cost of material purchases - how long is cash sitting in the form of inventory or materials vs money in your pocket? Discount volume pricing only works if your turns are quick. Otherwise, it is cash on a shelf that is worth less than the currency you bought it with.

What is your cash conversion cycle? How long does it take to recover your initial cash outflow?

Now What

Cash flow velocity is slowing down, and prioritizing cash management is more important than ever for businesses and non-profits during what looks to be a credit crunch and economic slowdown. I urge you to think about your own cash flow analysis and explore various strategies to improve your financial position.

Remember

Managing cash is how you create flexibility and freedom to Embrace Any Future! It’s never too late to get started.